Navigating Recurring Revenue Pitfalls: How Tokenization Shields Subscription Services from PCI Headaches

Navigating Recurring Revenue Pitfalls: How Tokenization Shields Subscription Services from PCI Headaches

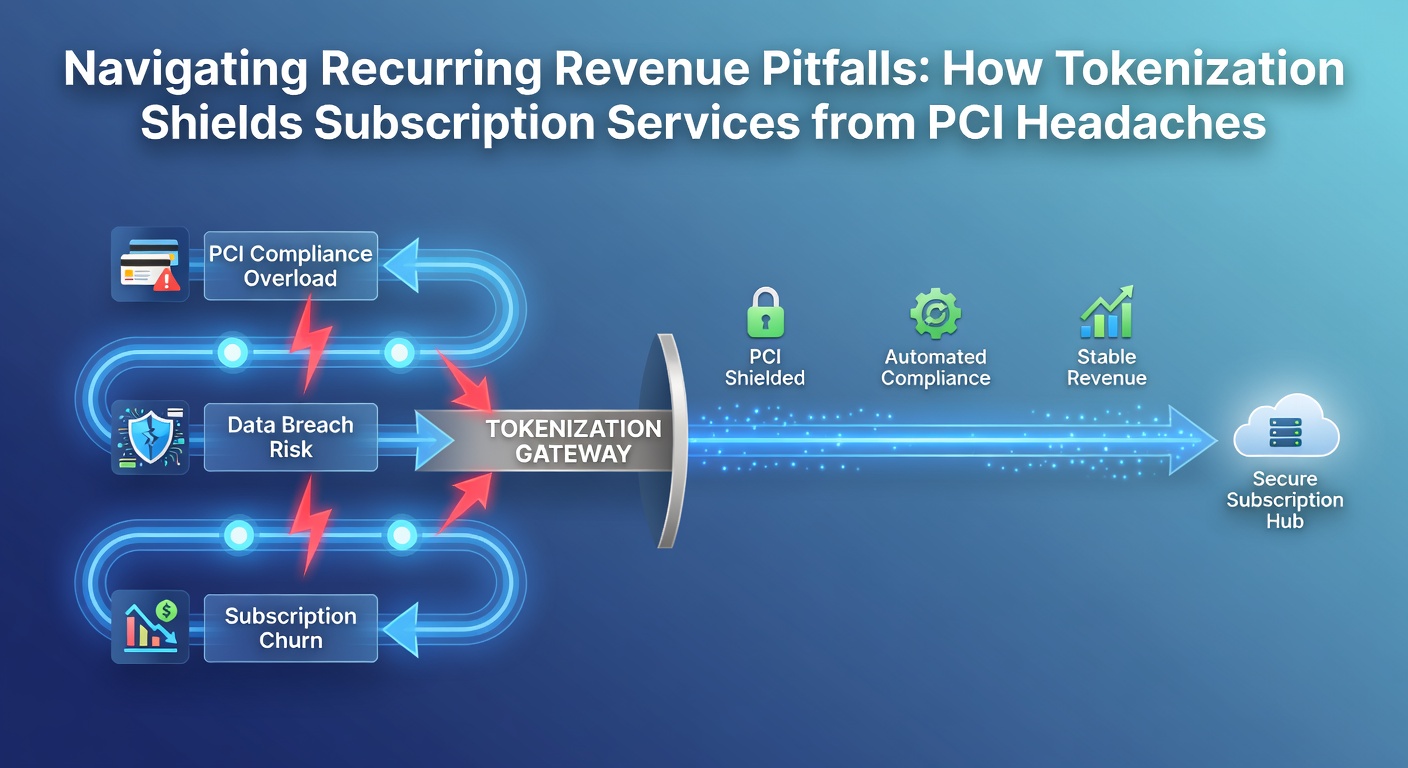

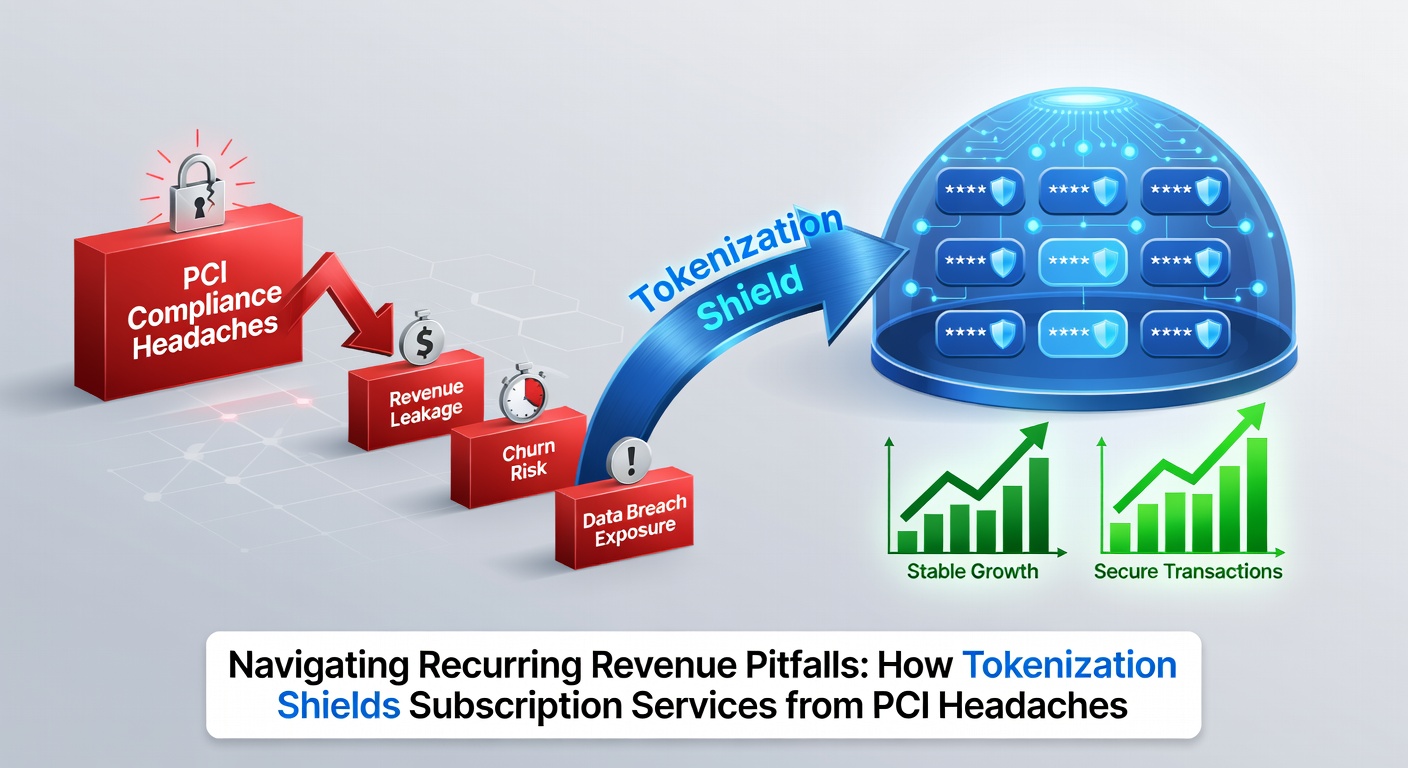

Subscription services have exploded in popularity over the past decade, powering everything from streaming platforms to meal kits and software-as-a-service tools, yet those managing recurring revenue streams often grapple with hidden pitfalls that threaten stability and growth. Failed payments disrupt cash flow; chargebacks erode margins; and compliance burdens, particularly around PCI Data Security Standard (PCI DSS), add layers of complexity and cost, especially since businesses handling card-on-file data for subscriptions must navigate stringent security requirements to avoid breaches or fines. But here's the thing: tokenization emerges as a proven shield, transforming raw payment data into secure, non-sensitive tokens that minimize exposure while streamlining operations for recurring billing.

The Subscription Boom and Its Sticky Underbelly

Figures from industry reports reveal that the global subscription economy surpassed $1.5 trillion in 2023, with projections climbing steadily as consumers embrace convenience over ownership, although operators face recurring revenue pitfalls like involuntary churn rates hovering around 20-30% annually due to expired cards, insufficient funds, or fraud attempts. Experts observe that subscription models rely heavily on stored payment credentials for seamless renewals, which exposes businesses to risks if those details fall into the wrong hands; data from the PCI Security Standards Council highlights how card-not-present transactions, common in subscriptions, account for over 80% of payment fraud incidents worldwide.

And while platforms promise dunning tools to retry failed payments, the real headache brews in the background with PCI compliance, demanding rigorous controls on cardholder data storage, transmission, and processing; non-compliance can trigger audits costing tens of thousands, or worse, massive fines up to $100,000 per month from acquirers enforcing these rules. Take one SaaS provider that overlooked vaulting customer cards properly: they faced a breach exposing 50,000 records, leading to six-figure remediation and lost trust that took years to rebuild.

PCI DSS: The Compliance Maze for Recurring Payments

PCI DSS sets 12 core requirements for any entity touching card data, from network segmentation to annual penetration testing, but subscription services hit unique snags because they store credentials long-term for automated billing cycles, pushing many into higher merchant levels with intensified scrutiny; research indicates Level 1 merchants, those processing over 6 million transactions yearly, endure quarterly on-site assessments that strain resources. What's interesting is how even smaller players, dipping into Level 2 or 3, must self-assess via lengthy questionnaires, often quarterly, while grappling with evolving threats like sophisticated skimming attacks targeting stored profiles.

Observers note that as of early 2025, the transition to PCI DSS 4.0 introduced custom security parameters and continuous monitoring mandates, ramping up pressure on subscription operators who previously skimmed by on legacy systems; and looking ahead to April 2026, when full enforcement of enhanced tokenization guidelines kicks in across major card networks, businesses without proactive measures risk deprioritization in processing queues or outright account terminations. Semicolons connect these dots: compliance isn't static, it evolves, forcing recurring revenue models to adapt or face escalating costs that data shows average $50-$100 per failed audit for mid-sized firms.

Tokenization Unpacked: From Raw Data to Impenetrable Tokens

Tokenization replaces sensitive card numbers with unique, randomized tokens—essentially stand-ins that hold no intrinsic value outside the issuing system's domain—allowing merchants to process recurring payments without ever storing, transmitting, or even viewing primary account numbers (PANs); processors like those aligned with Visa Token Service or Mastercard digital enablement generate these via APIs, mapping them server-side to real data only when authorizing charges. Turns out, this process slashes PCI scope dramatically, as tokens aren't considered cardholder data under PCI DSS, exempting vaulting services from most of the 12 requirements and reducing questionnaire lengths from hundreds to mere dozens of questions.

One study from a leading payments research firm found that businesses adopting network tokens saw PCI audit times drop by 40%, while breach risks plummeted since hackers stealing tokens gain nothing actionable; and for subscriptions, where renewals happen silently in the background, tokenized vaults enable instant retries without re-authentication prompts that frustrate users and spike churn. Experts who've implemented this note how it integrates seamlessly with billing platforms like Zuora or Chargebee, automating the swap from cards to tokens during initial signup and future updates.

Real-World Wins: Case Studies in Tokenization Triumphs

Consider a fitness app with 500,000 monthly subscribers that battled 15% churn from payment failures and looming PCI Level 2 audits; after partnering with a tokenization provider, they vaulted all profiles off-site, shrinking their compliance perimeter to near-zero while boosting recovery rates on declined renewals to 65%, according to internal metrics shared at industry conferences. That's where the rubber meets the road: tokenization not only dodges PCI headaches but enhances revenue capture, with data from Payments Canada showing tokenized recurring payments in North America reduce fraud losses by up to 60% compared to traditional card-on-file methods.

Another example involves a European e-learning platform navigating PSD2 strong customer authentication rules alongside PCI; by leveraging EMVCo-standardized tokens, they offloaded liability to issuers for most transactions, cutting chargeback rates in half and avoiding the multi-factor prompts that previously derailed 10% of subscriptions. Yet these aren't isolated wins—aggregators report that across sectors, tokenization lifts lifetime value per customer by 20-30% through fewer disruptions, all while sidestepping the audit marathons that plague non-tokenized setups.

Implementation Hurdles and Best Practices

Getting started demands choosing between gateway-hosted, merchant-hosted, or network tokenization—each with trade-offs like speed versus control—but the consensus among processors favors network tokens for their single-use security and cross-merchant portability, ideal for users switching services; integration typically spans 4-8 weeks via SDKs, with testing phases uncovering quirks like token expiration on card refreshes. And while initial setup costs $10,000-$50,000 for mid-tier operations, ROI materializes quickly through audit savings and churn reduction, as evidenced by benchmarks from payment orchestration platforms.

Those who've rolled this out stress regular token lifecycle management—provisioning new ones on card velocity checks or updates—to maintain efficacy, especially with April 2026 looming when card schemes mandate token exclusivity for high-volume recurring merchants in select regions, per updated operating regulations. Semicolon here: proactive firms audit token inventories quarterly, ensuring mappings stay current amid consumer card churn rates of 20% yearly.

Future-Proofing Subscriptions in a Tokenized World

By April 2026, expect accelerated adoption as PCI SSC's Tokenization Product Security Guidelines enforce stricter domain restrictions and key management protocols, compelling subscription giants to migrate legacy vaults en masse; research forecasts 70% of recurring billers will tokenize fully by then, driven by liability shifts that favor token holders in disputes. This shift promises smoother global expansion too, since tokens transcend borders without re-compliance hurdles, letting services like those in Australia or Canada tap unified vaults compliant with local mandates from bodies like the Australian Payments Network.

Now, smaller operators might balk at change, but scalable solutions from providers like Stripe or Adyen democratize access, bundling tokenization with analytics on payment health; the reality is, ignoring this leaves the ball in competitors' court, as tokenized models capture more renewals with less friction.

Conclusion

Tokenization stands as the linchpin for subscription services dodging recurring revenue pitfalls, transforming PCI compliance from a burdensome maze into a manageable backdrop while fortifying defenses against fraud and churn. Data underscores the transformation: reduced scopes, lower costs, higher recoveries—all converging to sustain the subscription engine that fuels modern businesses. Those embracing it early position themselves ahead, ready for regulatory waves like those cresting in April 2026 and beyond, ensuring steady revenue flows uninterrupted.