Inside Vendor Reconciliation Mechanics: How Online Payment Systems Streamline Settlements Across Diverse Merchant Categories in Platform Economies

Platform economies rely on intricate payment flows where vendors from retail, services, delivery, and freelance sectors receive settlements through centralized systems that handle thousands of transactions daily, and vendor reconciliation forms the backbone of accurate payouts by matching incoming funds against recorded sales, fees, and adjustments. These systems process data from multiple sources including card networks, digital wallets, and bank transfers while categorizing each merchant type according to its risk profile, transaction volume, and settlement frequency.

Core Mechanics of Automated Reconciliation

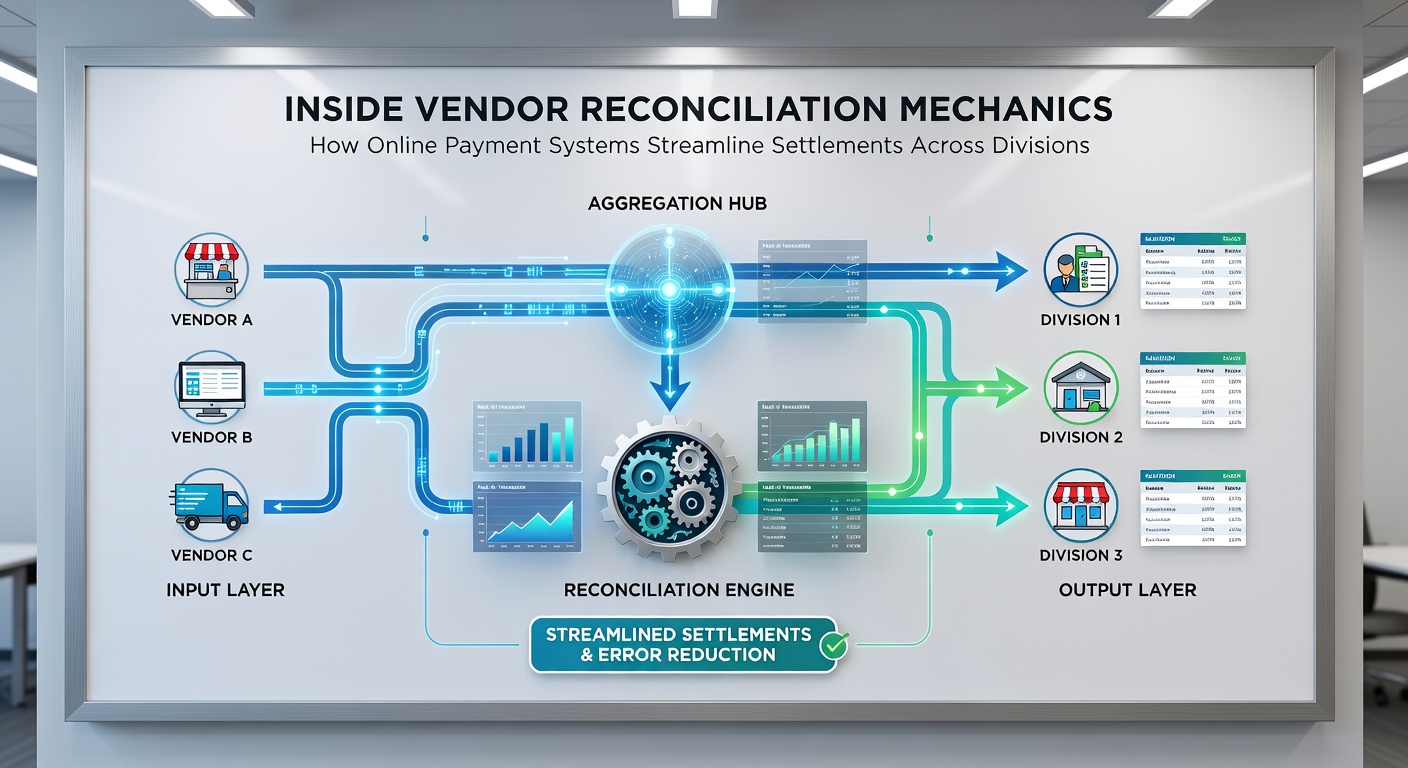

Online payment processors deploy matching algorithms that compare authorization records with captured payments and subsequent deposits, pulling data through APIs that connect directly to merchant databases and banking partners. Discrepancies such as chargebacks, refunds, or interchange fee variations trigger automated flags, which route to review queues where staff or rule-based engines apply corrections before final settlement batches run. This process runs on daily or weekly cycles depending on the platform agreement, and it incorporates currency conversion layers for cross-border vendors who operate under different regulatory frameworks.

Systems also segment settlements by merchant category so that high-volume retailers receive aggregated payouts minus processing fees, whereas gig economy participants see line-item breakdowns that reflect per-job earnings and platform commissions. Data from the Reserve Bank of Australia shows that automated reconciliation reduces manual intervention by up to 70 percent in large marketplaces, allowing platforms to scale across thousands of vendors without proportional increases in back-office staff.

Handling Diverse Merchant Categories

Retail merchants on platforms like e-commerce marketplaces generate high transaction counts with frequent returns, requiring reconciliation engines to reconcile inventory-linked sales against actual bank credits while isolating promotional discounts and tax withholdings. Service providers such as cleaning or consulting vendors submit fewer but higher-value invoices, so platforms integrate milestone-based triggers that release funds only after service confirmation, and the reconciliation layer verifies completion timestamps against payment rails.

Delivery and food platforms manage hybrid categories where drivers receive per-delivery payouts while restaurants settle on order aggregates, and payment systems apply separate fee schedules that the reconciliation software tracks through dedicated merchant identifiers. Observers note that these category-specific rules prevent cross-contamination of data, ensuring each vendor receives precise net amounts even when multiple revenue streams converge on a single platform account.

Integration with Platform Economy Infrastructure

Platform operators embed reconciliation modules within their core payment gateways so that vendor dashboards display pending, matched, and settled amounts in real time, and these interfaces pull live data from processors to show expected deposit dates. When platforms expand into new regions, the systems adapt to local clearing houses and compliance requirements by updating reconciliation parameters without rebuilding the entire settlement engine.

Industry reports from the Bank of Canada indicate that platforms using unified reconciliation tools achieve faster dispute resolution times because transaction histories remain centralized and timestamped, reducing the back-and-forth that occurs when data sits in separate silos. Vendors across categories benefit from this centralization because it supports predictive cash-flow modeling based on historical settlement patterns.

Regulatory Alignment and Data Standards

Payment systems incorporate compliance checkpoints during reconciliation to verify that tax withholdings and reporting thresholds align with jurisdiction-specific rules, and this becomes especially relevant for platforms operating across multiple countries where vendors fall under different reporting regimes. European Central Bank guidelines on payment data emphasize standardized reporting formats that facilitate cross-border reconciliation while protecting sensitive merchant information through encryption and access controls.

These standards also cover anti-money laundering screening that runs parallel to financial matching, ensuring flagged transactions receive additional scrutiny before funds release. Platforms that maintain audit trails within their reconciliation systems can demonstrate compliance during periodic reviews without reconstructing records from disparate sources.

Conclusion

Vendor reconciliation in platform economies continues to evolve through tighter API connections, improved matching logic, and category-aware rule sets that accommodate retail, service, and gig participants under one infrastructure. As settlement volumes grow, the emphasis remains on accurate matching, timely adjustments, and regulatory alignment that keeps payouts reliable across diverse merchant profiles. Projections tied to industry updates expected around May 2026 point toward further standardization of data formats that will streamline these processes even more.